Running a jewelry store means watching customers fall in love with pieces they can't immediately afford. The $8,500 engagement ring, the anniversary necklace at $3,200, the custom wedding band set — these purchases need financing options. But the operational mess that follows when you offer layaway or payment plans can quietly destroy your cash flow faster than a bad holiday season.

Most jewelry stores handle financing through a patchwork of spreadsheets, sticky notes, and whatever their POS system half-supports. Missing payments slip through for weeks. Items sit in hold status limbo. Staff manually chase down customers who've defaulted. And reconciliation turns into a monthly nightmare where nobody really knows which payments belong to which contracts.

The real damage happens quietly. A customer on a 6-month layaway for a $4,800 bracelet misses month three. Your staff doesn't catch it until month four because the tracking lives in someone's personal Excel file. Now you're holding dead inventory while chasing a customer who's probably not coming back. Meanwhile, someone else wants that exact piece — but your system shows it as "sold" even though you haven't collected half the money.

Contract fields that actually prevent disputes

Standard jewelry layaway workflow starts with the contract, and most stores use generic templates that miss critical operational details. You need specific fields that protect both your inventory and cash flow.

The basics — item description, price, down payment, payment schedule — aren't enough when you're dealing with high-value pieces and extended terms. Your contract needs operational triggers built in.

Start with hold classification fields. A layaway item isn't just "on hold." It needs status markers that tell your team exactly where it stands. Standard 90-day layaway? 6-month payment plan with possession? Special-order item awaiting final payment? Each classification needs different handling rules, and mixing them up costs money.

Payment milestone fields matter more than payment amounts. Instead of just listing "$800 monthly for 6 months," your contract should mark critical decision points. Month 3: eligibility review for extension. Month 4: automatic conversion to available inventory if behind. Month 5: final notice before forfeiture. These aren't just dates — they're operational triggers that keep items from sitting in limbo.

Default penalty structures need absolute clarity, but not in legal language. Skip the fine print about "acceleration clauses" and spell out what actually happens: "Missing two payments means losing your 30% deposit and the item returns to floor inventory within 72 hours." Customers understand that. Courts understand that. Your staff can actually enforce it.

POS hold flags that prevent phantom inventory

Your POS system probably has basic hold functionality, but jewelry layaway workflow needs multiple flag types that standard retail systems don't really support. The difference between "layaway hold" and "payment plan hold" isn't semantic — it changes how you handle everything from insurance to inventory counts.

Never miss a sale or shipment again.

Jewlyly helps you manage orders, track inventory, and engage customers seamlessly.

- Real-time inventory tracking

- Automated customer notifications

- Sales and order analytics

No credit card required

Layaway holds mean the item stays in your safe but out of available inventory. These pieces need special handling during physical counts because they're technically sold but not yet delivered. Most POS systems treat them as regular inventory with a note, which leads to confusion during reconciliation. You need a flag that removes them from sellable stock while keeping them in your possession tracking.

Payment plan holds work differently when customers take possession after hitting a certain threshold — usually 50-60% paid. Now you're tracking an item that's physically gone but financially incomplete. Your system needs to show this as a receivable asset, not inventory. Mixing these up throws off your reorder points and makes insurance claims a headache.

Then there's the partial payment hold for custom orders. A customer puts $2,000 down on a $7,000 custom piece that won't exist for 8 weeks. This isn't inventory at all — it's a liability until you create and deliver the piece. But most stores track it like a regular layaway, creating phantom inventory that messes up open-to-buy calculations.

The worst mistakes happen during status transitions. A customer on layaway decides to finance the remaining balance through a third party. Your POS needs to handle the shift from internal hold to external financing without losing the payment history. Most systems require manually closing one transaction and opening another, losing critical data in the process.

Payment schedules that match customer behavior

Theoretical payment schedules look clean on contracts. Week one: $500 down. Months 1-5: $400 each. Month 6: final $300. Reality looks different. Customers pay early, pay late, pay in weird amounts, and your system needs to handle all of it without breaking.

The traditional approach locks customers into rigid monthly payments on specific dates. Miss the date, trigger a late fee. But jewelry purchases are emotional, expensive decisions — and your payment structure needs to accommodate how people actually pay for luxury items.

Flexible window scheduling works better than fixed dates. Instead of "due on the 15th," create payment windows: "Payment 2 due between days 25-35." This gives customers breathing room while keeping your collections predictable. A customer getting paid on the 1st and 15th can pick their best timing without technically being late.

Accelerated payment incentives change the cash flow picture. Offer 3% off the remaining balance if paid in full before month 4 of a 6-month plan. Roughly a third of customers will take it, improving your cash position without discounting the original price. But your system needs to automatically calculate and apply these incentives, or staff will mess up the math.

Amount flexibility within bounds prevents defaults while protecting margins. Let customers pay 80-120% of their scheduled payment without penalty or prior approval. Someone scheduled for $400 might pay $320 one month and $480 the next. As long as they're trending toward completion, rigid enforcement just creates friction. Your tracking system needs to show whether they're ahead, on track, or falling behind based on cumulative payments — not individual installments.

Here's a practical payment schedule structure that actually works:

| Component | Traditional Approach | Flexible Approach | Operational Impact |

|---|---|---|---|

| Payment Timing | Fixed monthly date | 10-day window | 65% fewer "late" payments |

| Payment Amount | Exact amount only | 80-120% flexibility | Reduces partial payment confusion |

| Early Completion | No incentive | 3-5% discount | ~30% take rate, faster cash recovery |

| Grace Period | 5 days, then fees | Built into window | Eliminates most dispute calls |

| Catch-up Options | Penalty-based | Payment plan reset | Keeps customers engaged vs defaulting |

The traditional approach locks customers into rigid monthly payments on specific dates. Miss the date, trigger a late fee. But jewelry purchases are emotional, expensive decisions — and your payment structure needs to accommodate how people actually pay for luxury items.

Default handling that recovers value

Defaults happen. The engagement ring purchase falls through. Job loss hits. Priorities change. Default rates in jewelry layaway hover around 15-20%, and they run higher on pieces above $5,000. How you handle them determines whether you recover value or eat losses.

Most stores follow a passive default process: wait, send letters, eventually return items to inventory. By then, months have passed, the piece might be out of season, and you've had capital tied up the whole time. Active default management recovers more value, faster.

The 45-day rule helps a lot. At 45 days past due, immediately convert the item status from "held" to "at-risk inventory." Don't release it for sale yet, but flag it for special handling. Your sales team can mention it to qualified customers as "potentially available soon." This creates urgency with the original buyer while identifying backup buyers.

Contact escalation should be operational, not emotional. Days 1-15 late: automated text reminder. Days 16-30: phone call from the associate who made the sale. Days 31-45: manager call with resolution options. Day 46 and beyond: formal default notice with clear next steps. Each stage needs different messaging and different staff involvement.

-

Days 1-15 late

automated text reminder.

-

Days 16-30

phone call from the associate who made the sale.

-

Days 31-45

manager call with resolution options.

-

Day 46 and beyond

formal default notice with clear next steps.

Recovery options beyond "pay or lose" keep customers engaged. Offer to convert the layaway to a lower-priced item using accumulated payments as credit. Switch from layaway to financing if they qualify. Transfer the contract to a family member. These alternatives recover something versus nothing, and your system needs to handle contract modifications without starting from scratch.

Once forfeiture is triggered, execute fast: photograph the item, document its condition, record all payment history, issue formal forfeiture notice, return item to inventory within 72 hours. The longer you wait, the more likely disputes become. Quick execution actually reduces customer complaints — there's no ambiguity about what happened.

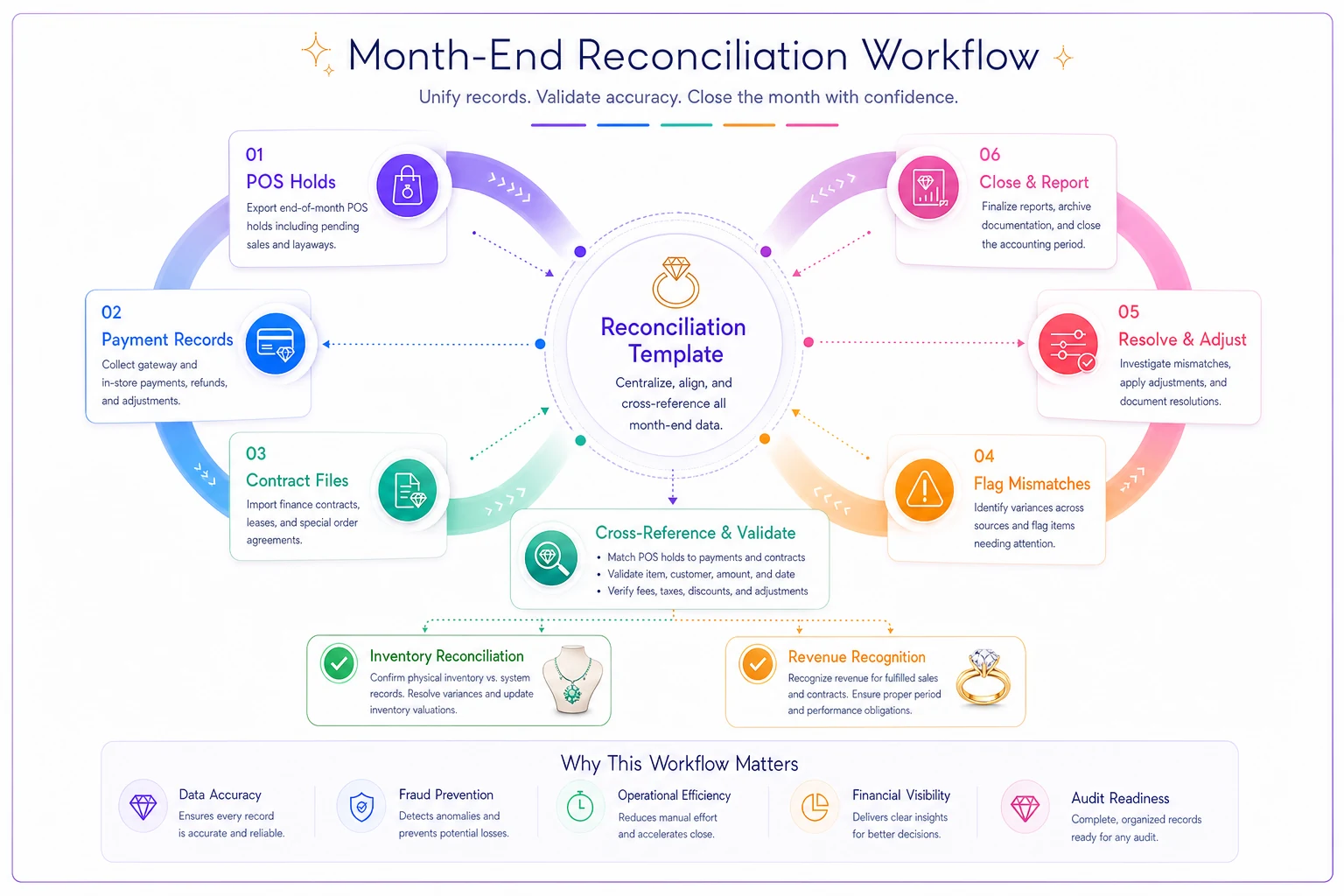

Reconciliation templates for complex payment arrangements

Monthly reconciliation for jewelry layaway workflow is a multi-dimensional puzzle. You're tracking partial payments across dozens of contracts, each with different terms, statuses, and progression rates. Generic accounting software can't handle it. Neither can basic POS reports.

Build reconciliation templates that separate different payment types from the start. Layaway payments, financing payments, partial custom order payments, and deposit forfeitures all need different treatment in your books. Mix them together and you won't spot problems until they're already large.

A working reconciliation template tracks four key dimensions:

Payment Status Progression: How many contracts moved from one stage to another this month? If you started with 45 active layaways and ended with 52, where did the 7 new ones come from, and how many completed or defaulted? This flow analysis spots bottlenecks before they become cash flow problems.

Revenue Recognition Timing: Layaway revenue doesn't hit your books until delivery, but financing might recognize partially depending on your terms. Custom orders recognize at different points depending on your policy. Your template needs separate columns for collected cash versus recognized revenue — and they won't match.

Inventory Status Alignment: Every held item needs a corresponding payment contract, and every contract needs accurate payment tracking. Your reconciliation should flag mismatches — items marked "sold" with no payment activity, contracts showing balances with no inventory assigned, or completed payments with items still on hold.

Aging Analysis by Category: Standard aging reports don't work for payment plans. You need aging by contract start date, last payment date, and expected completion date. A 4-month-old layaway that's 60% paid is healthier than a 2-month-old one that's only seen the deposit.

A working reconciliation template tracks four key dimensions:

Real reconciliation workflow example

Walk through an actual month-end reconciliation for a store with 47 active payment arrangements. March closes with $67,000 in expected payments across all contracts. Here's what actually happened:

Collected payments totaled $58,500 — looks like you're behind. But drilling into the template shows the real story. Three customers paid their contracts in full early (you expected $4,800, received $14,200 from them). Five customers missed payments entirely ($6,300 expected, none collected). The rest paid within their windows but at varying amounts.

The inventory reconciliation turns up two problems. A tennis bracelet shows as layaway-held but has no active contract — someone forgot to clear the hold when the customer cancelled in February. Meanwhile, a contract for $3,400 shows active payments but the ring is marked as available inventory. That's a dangerous mistake that could lead to double-selling.

Your template catches these because it cross-references three data sources: POS holds, payment records, and contract files. Manual reconciliation would take hours and miss half of it.

Here's a quick visual of that reconciliation workflow.

Your template catches these because it cross-references three data sources: POS holds, payment records, and contract files. Manual reconciliation would take hours and miss half of it.

Technology integration for jewelry payment plans

The operational complexity of custom order deposits and milestone templates that reduce disputes shares a lot with layaway management — both need sophisticated tracking beyond what standard POS systems provide. The difference is that layaway adds inventory holding costs and default risk to the mix.

Modern jewelry stores need systems that connect contract management, payment processing, inventory tracking, and customer communication. Full enterprise systems cost more than most independent jewelers can justify. The solution isn't buying bigger software — it's building better workflows that standard tools can actually execute.

AI automation helps by handling the repetitive coordination tasks that usually fall through the cracks. Payment reminder sequences, status updates, escalation triggers — these don't need human judgment, just consistent execution. An AI-powered operational platform can monitor payment patterns and flag accounts likely to default before they actually miss payments, giving you time to intervene early.

The real value comes from centralizing information that usually lives in separate systems. When your contract terms, payment history, inventory status, and customer communication all live in connected workflows, reconciliation becomes automatic instead of archaeological. You stop losing track of contracts, stop miscounting held inventory, and stop surprising customers with forfeiture notices they didn't see coming.

Margin protection during payment arrangements

Extended payment terms create hidden margin erosion beyond just default risk. You're effectively financing purchases at zero percent while your costs keep climbing. With precious metal pricing volatility, a 6-month layaway on gold jewelry might cost you 8-15% in replacement cost increases alone.

Smart operations build margin protection into the payment structure itself. Price locks need expiration dates — guarantee the price for 90 days, then reserve the right to adjust for market changes. This isn't about gouging customers; it's about not selling at a loss when gold jumps $200 an ounce during their payment plan.

A realistic scenario: a customer starts a layaway in January for a $4,500 gold necklace, planning to complete payment by June for an anniversary. Gold rises 12% by April. Your replacement cost is now $5,040, but you're locked into the original price. That's $540 in margin erosion on a single piece.

The operational fix isn't complicated, but it needs systematic execution. Build price adjustment triggers into your contracts — if precious metal prices move more than 10%, you can offer the customer three options: pay in full at the original price within 30 days, accept a price adjustment on the remaining balance, or cancel with a full refund of payments made. Most choose option one, which accelerates your cash flow.

Workflow optimization for staff efficiency

The daily workflow of managing jewelry layaway programs kills productivity when handled manually. A store with 40-50 active payment plans easily needs someone spending 2-3 hours a day just on payment tracking, customer communication, and status updates. That's close to a part-time position worth of work that usually gets squeezed into everyone's "spare time."

Streamlined workflow starts with daily dashboards, not hunting through spreadsheets. Every morning, your team should see: payments expected today, contracts at risk of default, items ready for pickup, and any status changes from the day before. That's a 5-minute review instead of a 45-minute compile.

Task assignment based on contract stage prevents dropped balls. New layaways go to the selling associate for relationship management. Payment issues go to office staff for resolution. Final pickups return to sales for completion and potential upsell. When everyone knows their role at each stage, nothing sits in limbo waiting for "someone" to handle it.

Batch processing similar tasks multiplies efficiency. Instead of handling each payment as it arrives, process all daily payments at 2 PM and 6 PM. Instead of making late payment calls at random, block Tuesday and Thursday mornings for collections. This rhythm reduces context switching and improves consistency.

Block specific daily times for batch payment processing (for example, 2 PM and 6 PM) to reduce context switching and improve consistency.

Batch processing similar tasks multiplies efficiency. Instead of handling each payment as it arrives, process all daily payments at 2 PM and 6 PM. Instead of making late payment calls at random, block Tuesday and Thursday mornings for collections. This rhythm reduces context switching and improves consistency.

The real cost of manual layaway management

Some honest math about what poor layaway workflow actually costs. Take a typical independent jeweler doing $1.2 million annually with 20% of sales through payment plans. That's $240,000 in extended payment transactions, usually across 150-200 contracts per year.

With a 15% default rate, you're looking at $36,000 in potential losses — and that assumes you catch defaults immediately and return items to inventory fast. In reality, pieces sit in limbo for weeks. If those items could have sold at full price but instead get cleared out at 30% off after a failed layaway, your real loss doubles.

Add staff time at roughly 3 hours daily for management — around $22,000 annually in labor. Payment processing confusion leading to reconciliation errors: maybe $5,000-8,000 in write-offs and corrections. Customer disputes from unclear contracts or miscommunication: another few thousand in discounts and reputation damage.

You're looking at $70,000-80,000 in total cost for what seemed like a simple customer service offering. That's 6-7% of total revenue evaporating into operational inefficiency.

Building proper workflows with clear contracts, automated tracking, and systematic default handling cuts this by more than half. The technology exists — whether through enhanced POS features, dedicated layaway management tools, or AI-powered operational platforms that connect your existing systems. The question isn't whether you can afford to upgrade your jewelry layaway workflow. It's whether you can afford not to.

The stores succeeding with payment plans aren't the ones with the most generous terms or the lowest deposits. They're the ones with operational systems that handle complexity without requiring heroic effort from staff.

Build those systems, and payment plans stop being an operational burden and start being a real competitive advantage.

Ready to elevate your jewelry store operations?

Join 500+ jewelers using Jewlyly to increase efficiency, reduce errors, and grow revenue.